European Geologist Journal 44

Resource sustainability – Geology is the solution

by Eamonn F. Grennan and John A. Clifford

Contact: eamonn.grennan@outlook.ie

Abstract

The question of resource sustainability was developed during the late 1960s and lies at the core of a number of alarmist reports compiled at that time, none of which had a geological perspective. The public perception of geology is that it has little, if any, impact on their everyday lives. This is, of course, a fallacy. Geology is one of the central factors that impacts, and needs to be considered, across a range of public policy issues and it is noteworthy that in all of these reports exploration risk is never considered. At present Europe is dependent on imports of raw materials from countries which do not necessarily have good environmental standards. If Europe really wants a quality environmental future, it must encourage the discovery of its own resources and not develop policies that inhibit their development. Europe can only ensure a secure, and sustainable, supply of raw materials for its industrial base by doing this.

As with many scientific arguments, the actual starting date and the person, or persons, responsible for the idea of ‘resource sustainability’, is usually a matter of great debate. We propose to use just four principal references. Our starting point is “A Report for the Club of Rome” (Meadows et al. 1972), using the abstract established by Pestel (no date). Their model “was built specifically to investigate five major trends of global concern”, including “the depletion of non-renewable resources”. The latter statement goes to the core of the sustainability debate.

As a matter of fact, the Earth is of a certain size with a fixed amount of materials. Thus, from a fundamentalist point of view, the extraction, use and discarding of non-renewable raw materials lessens the amount available for future use. This is a fundamentalist position based primarily on the supposition that all resources have been discovered. To take just one example, the total amount of gold produced in the world is about 187 kt (World Gold Council website 2017). No one is suggesting that we are running out of gold. No, geology is not the problem.

Over the past 50 years we have witnessed many transient shortages of materials such as germanium, gold, zinc, rare earths, and even iron, as well as those others listed in the Critical Raw Materials (CRM) reports. In parallel with this is the changing demand for materials and the use of substitutes, e.g. hematite was substituted for 20% of the barite in drilling mud, fluorspar was in high demand in the steel industry during the 1970s and mines opened and closed due to major price variations. In the latter case, due to recent increase in demand, fluorspar is now designated as a CRM. Demand for, and the price of, gold has fluctuated widely during the past 50 years; copper prices rose and fell with economic activity; iron ore prices rose rapidly for a period in the late 20th century due to demand, principally, from China; all are examples of supply and demand.

We concur with the CRM report that “Raw materials are fundamental to Europe’s economy, growth and jobs and are essential for maintaining and improving our quality of life” (CRM, 2014:7). However, only “around 9% of raw material supply is indigenous to the EU” (p.30) “largely due to industrial minerals production” (p.8, authors’ emphasis). The CRM notes that “total supply across all twenty raw materials can be estimated at less than 3%, with over half having no, or very limited, production within the EU” (p.30).; with 14 of the 20 imported from China.

The rationale behind the CRM 2010 Report was refined in the 2014 report suggesting that while “most of these metals and minerals will continue to be imported from sources outside Europe; others can, and should be produced domestically” (CRM, 2014:8). In implementing such an action, we agree with Brundtland (1981) that the ecological ramifications must be considered at the same time as the economic, trade, energy, agricultural and other dimensions. As is pointed out in the CRM (2014), the problem is that the environmental considerations now have a veto on resource development in Europe to the detriment of the environment and sustainable development of Less Developed Countries (LDCs).

Shortages/sustainable supply

It would seem from study of the CRM document that the primary issue for the EU is to secure a sustainable, reliable and continuous supply of resources without a discordant pricing policy. As enunciated in the ERA-MIN (2017), and reflecting Brundtland (1981), the question of finite resources is a non-issue and the objective should be to “secure sustainable supply of raw materials, increasingly from European sources.” This is in accordance with the aim of the European Industrial Policy (EIP). There are of course a number of supply problems, the rate of discovery for some materials may not be fast enough or the difficulties, be they metallurgical, financial, environmental, or administrative, may not be resolved in a timely manner.

We agree with Brundtland (1981) that efficiencies and recycling technological advances are important with the caveat that in many instances such advances will involve the use of different raw materials, which are as yet undiscovered. In addition, it is likely that the sophisticated chemistry required in the production of the newer materials will probably lessen their suitability for recycling.

Thus, Brundtland (1981) is correct in arguing that “the integration of environment and development is required in all countries, rich and poor” (Ch. 1, para. 48) and in pointing out that “economic growth always brings risk of environmental damage” (Ch. 1, para. 50). Those risks can be, and are being, addressed in all new mining ventures, which require a closure plan as part of the development application. We must recognize however that, as Commissioner Hogan has stated in another context, “you cannot make an omelette without breaking eggs”!! (Hogan, 2014). What we must argue against is that Europe is exporting the mining industry to LDCs, importing the raw materials and then selling the end product back to the LDCs.

Geology, exploration, and risk

Fundamental to a sustainable supply of raw materials for manufacturing industry is a mining industry; fundamental to a sustainable mining industry is a vibrant exploration industry; fundamental to a vibrant minerals exploration industry is geology. The real problems of the technical and financial risk attaching to mineral exploration, and the importance of geology, are rarely discussed.

To take just one simple example: Ireland is a major zinc concentrate producer in Europe and is in the world’s Top 15 (E. Doyle pers. comm. 2017). All of the deposits which have contributed to this achievement have been discovered within 100 m of the ground surface. During the process of mining, the deposits have been extended to greater depths, some in excess of 300 m. Nobody is seriously suggesting that discovery depths of 100–200 m will not happen. Of course, the cost of discovery will be greater and indeed such is the confidence in making another discovery that expenditure on exploration in Ireland in the period 2012–2016 was nearly EUR 100 million (E. Doyle pers. comm. 2017), over 90% of which was directed to zinc.

There are two principal reasons why exploration tends to be ignored in all of this debate. Firstly, the high risk of no success – exploration success in Ireland is around 5,000 to 1. Most people, especially those in government service or in academia, rarely understand why anyone would undertake such risks. This is why there is a special section within the Stock Exchanges for such high risk companies. Secondly, having succeeded in finding a viable deposit, the extent of the regulatory obstacles put in the way of development is enormous, and costly. They can be ameliorated, but the environmental lobby has totally captured the administrative system.

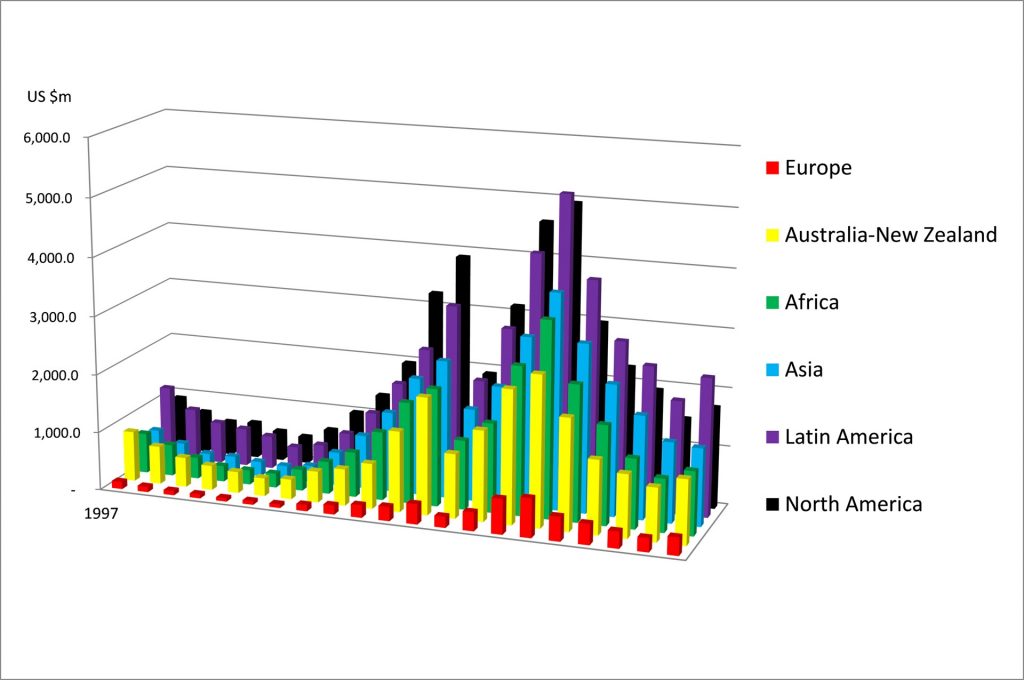

Some countries in Europe, including within the EU, had a vibrant metals exploration and mining industry until the early 1960s. Today, however, the mining of metals has virtually ceased in most countries in the geographic core of Europe and has continued elsewhere only at a low ebb. This, we suggest, is a result of policy changes at both EU and corporate level. This is highlighted by the global distribution of exploration expenditure over the past 20 years, demonstrating the unsustainable low level of exploration investment in Europe relative to other regions (Figure 1).

Figure 1: Global Distribution of Exploration Expenditure, 1997 –2017 (SNL Database).

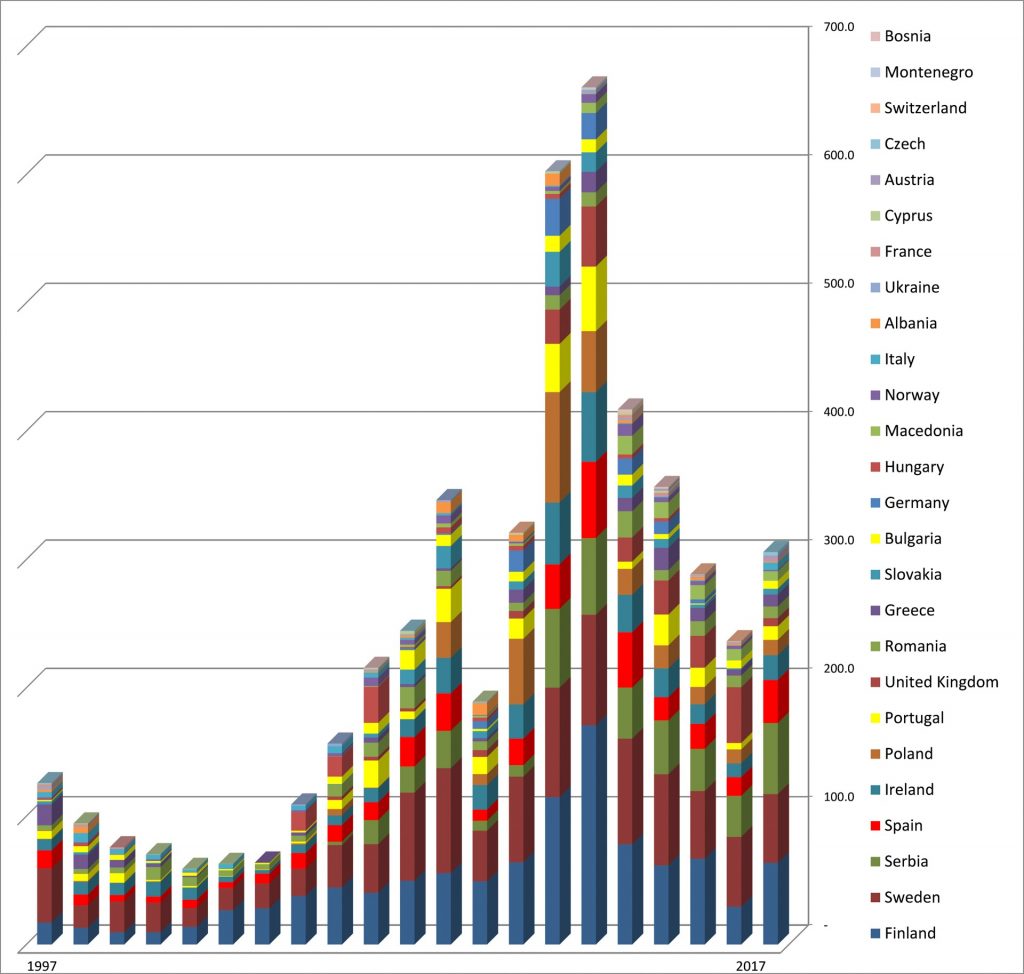

This point becomes even more obvious when it is realised that 50% of the European exploration expenditure is focused on just three countries – Finland, Sweden and Serbia – with a further 25% in the next four countries – Spain, Ireland, Poland, and Portugal (Figure 2). It is more than coincidence that significant new base metal discoveries, or extension to existing operations, have been made in each of those countries during the past decade.

Figure 2: European Exploration Expenditure (million USD) Distribution, 1997–2017 (SNL Database).

Principally within English speaking countries, minerals exploration and mining are two distinct sectors. Both have major financial risks – does the deposit being sought exist? – and the world is full of examples of mining projects which went wrong for a wide variety of reasons including, inter alia, poor timing, substitution by other commodities and over-extended loans. Within centrally controlled economies and most of the non-English speaking countries in the EU, exploration is undertaken either by a State agency or a mining company, either directly or by funding a junior partner. So the true cost of exploration and the very high risk attaching to it is not appreciated.

An understanding of the need for a separate high risk exploration psyche is essential for the discovery of new deposits. We consider that the excellent admonition of the need to incentivise European production of critical raw materials (20th May 2014 Press Release accompanying the publication of the CRM) is fundamental to finding the answer to a sustainable supply, with the caveat that “production” captures both the exploration and mining industries.

It has been argued that the best, and most efficient, way to find a deposit is to allow small exploration companies to flourish, whereby they can raise high risk finance and/or obtain exploration funding from major mining companies. Whilst it is undoubtedly true that exploration costs are rising, the real escalation in costs is in the post-discovery pre-development phase. Few geologists will argue against an increase in environmental and reporting standards, and inevitably the smaller company cannot sustain the costs and is typically taken over by the larger partner. The major company, through social and regulatory pressure accedes to the environmental/cultural/administrative lobby. This in turn leads to increased costs being imposed both directly and indirectly on the developer, which leads to lower profits, and thus lower tax payments, resulting in the self-fulfilling prophecy that such companies avoid paying tax. This does not have to be the case, as is shown by the recent Australian case studies, such as the Nova and DeGrussa deposits, which went from discovery to production in 2 and 3 years respectively.

The INTRAW Report (2017) on Industry and Innovation suggests that new discoveries will likely be at depths in excess of 200 m, that new geological concepts and exploration technologies will be required to detect them, and this at a time when European universities and research institutes are either closing, or have declining interest in the geosciences. This view is further reflected by ERA-MIN (2013) which stresses that “research is vital to explore for deeper-seated deposits”. We agree with these opinions, but note that “deep” in this context can mean “blind”, in that new discoveries, such as Sakatti (Coppard, 2011), will be made beneath peat bogs and cover rocks, often at depths significantly less than 200 m.

Europe needs an exploration industry that is likely to succeed in discovering an economically exploitable resource. There exist sufficient data today in general geology, structural geology, geochemistry or geophysics. These should be made available to small companies and within a system that gives the explorer rights.

Geologists, research and education

With some notable exceptions, geologists are poor communicators, and rarely participate in public policy debate. Indeed, even within corporate structures they are seldom heard outside of their chosen profession. Thus, when major over-arching studies are being compiled they are seldom if ever on the steering committee and often do not make it onto the important consultative committees. This lies at the root of many of the exaggerated statements of dwindling resources, and of the failure in communication of the value that geology brings to society.

Fortunately, this problem of public engagement has been recognized by certain geological organisations, of which the EFG is one, and which is also being addressed by some excellent television specials, as for example the Iain Stewart presentations on the BBC. However, more needs to be done.

In Ireland, the government is proactive through the Science Foundation Ireland in sponsoring, with a 5-year, EUR 25 million grant, to iCRAG – a geological research centre, and also in funding the Geological Survey of Ireland (GSI) to carry out a nationwide geochemical and airborne geophysical programme, code named TELLUS. Both of these initiatives will bear fruit in the future and reflect the ERA-MIN recommendations on the support required by the traditional and high-technology industries in Europe.

Unfortunately, at the very time when specialist and well-honed skills are required, the greying of the exploration community and a trend for new, graduate geologists to preferentially choose careers in sectors of the geosciences which do not require extended field time, mean that there is increasing loss of ‘corporate knowledge’ and the mentoring required in the passing on of critical exploration and mining skills.

Further, the majority of ERA-MIN activities are restricted to the academic and government domains, while links with the private sector are, with some notable exceptions, poorly developed, thus resulting, we contend, in a lack of research focus.

SMEs generally do not have a record of implementing high cost exploration. Such programs, which often require major academic input, only suit large companies. A similar issue applies to the exploration for deep deposits. In this respect, it can be stated that the so-called traditional methods have not been systematically applied over much of Europe.

To address this problem, grant aid programmes need to have a grant level below which the administrative procedures are relaxed for SMEs. The concept of taxation credits to facilitate the initial evaluation of prospective areas is another idea worthy of consideration.

Way forward

The lingering negative perception of mining is a matter that must be addressed. In addressing it, it needs to be emphasized that successful exploration is a pre-requisite for a mining project. Interestingly the opponents of mining are far more cognisant of this fact and this is why they lobby against any incentives for exploration. In the absence of such incentives there will be no exploration.

The recent removal of environmental protection over part of the Amazon Basin was greeted with horror by the environmental community. This decision, at least in part, is an unintended consequence of the EU’s outsourcing of its raw material requirements, rather than developing indigenous sources of supply, and thereby results in the exporting of the problem of mine waste management. As pointed out by Brundtland (1981) environmentalists must recognize that their policies can have adverse consequences.

Under a series of EC generated Directives, most Member States have adopted a series of environmental regulations which make it very difficult or even virtually impossible, to develop a mineral deposit. There is no balance, only the environmental aspects are given a veto; whilst the broader benefits for society are not given the same weight or credence. Thus, the EUs industrial heartland, built on hundreds of years of mining and manufacturing, now exists only as a manufacturing hub. It is worth recording that some 30 million jobs in the EU are directly reliant on access to raw materials (CRM, 2014).

The ERA-MIN roadmap lists four key areas that need to be addressed – exploration; mining/quarrying; mineral processing and metallurgy; mine closure and rehabilitation. If the ERA-MIN roadmap objectives are to be realised in the exploration sector then we need: access to lands to carry out exploration; new geological, geophysical and geochemical data to support that exploration, and financial incentives to attract mobile exploration funding.

One of the oft quoted sentences from Brundtland (1981) is “humanity has the ability to make development sustainable – to ensure that it meets the needs of the present without compromising the ability of future generations to meet their own needs”. This goes to the core of what is required in Europe; we must develop our own sustainable resources.

Acknowledgements

The authors wish to thank Gareth Ll. Jones, Christian Schaffalitzky and Garth Earls for reviewing an early edition of this paper.

References

Brundtland, G.H. 1981. United Nations, (1987) Our Common World Commission on Environment and Development, Oxford University Press.

Coppard, J. (2011). Sakatti – Copper-Nickel-PGE Exploration Target, Sodankyla Region, Finland. Anglo American Exploration Fact Sheet, November 2011.

CRM. 2010. Critical Raw Materials for the EU (CRM), Report of the Ad-hoc Working Group on defining critical raw materials. European Commission.

CRM. 2014. Report on Critical Raw Materials for the EU. European Commission (COM(2014) 297 final ).

ERA-MIN, 2013. http://www.era-min-eu.org/

Hogan, P. 2014. Public statement to reporters, 15 January. www.thejournal.ie

INTRAW Project. 2016. Operational Report: Education and Outreach. http://intraw.eu/wp-content/uploads/2017/03/INTRAW_WP1_Transactionalreport_E-O.pdf

INTRAW Project. 2016. Operational Report: Research and Innovation. http://intraw.eu/wp-content/uploads/2017/03/INTRAW_WP1_Transactionalreport_R-I.pdf

Meadows, D.H., Meadows, D.L., Randers, J., Behrens III, W.W. 1972. The Limits to Growth: A Report to the Club of Rome. New York: Universe Books.

Pestel, E. (no date). Abstract of Limits to Growth, A Report to the Club of Rome. Propagandamatrix website (accessed August 2017)

Poirier, C. (no date). Amazon Watch, quoted in The Week, 2 September 2017 (Issue 1140). London: Dennis Publishing Ltd.

World Gold Council website (accessed 14 September, 2017). http://www.gold.org/search/site/187

This article has been published in European Geologist Journal 44 – Geology and a sustainable future.

Read here the full issue: